After years of disruption, travel demand is proving far more resilient than many expected, particularly in the premium and group segments.

Global RevPAR (Revenue per Available Room) continues to rise, driven by strength in international markets and the recovery of business travel.

U.S. group bookings are tracking ahead of last year's pace, and international travel to the U.S. is on the rise.

At the same time, industry leaders are expanding their footprints, consolidating brands, and building out robust loyalty programs to capture repeat customers.

All of this is happening while supply growth remains constrained by elevated construction costs and tighter financing, which supports pricing power for the incumbents.

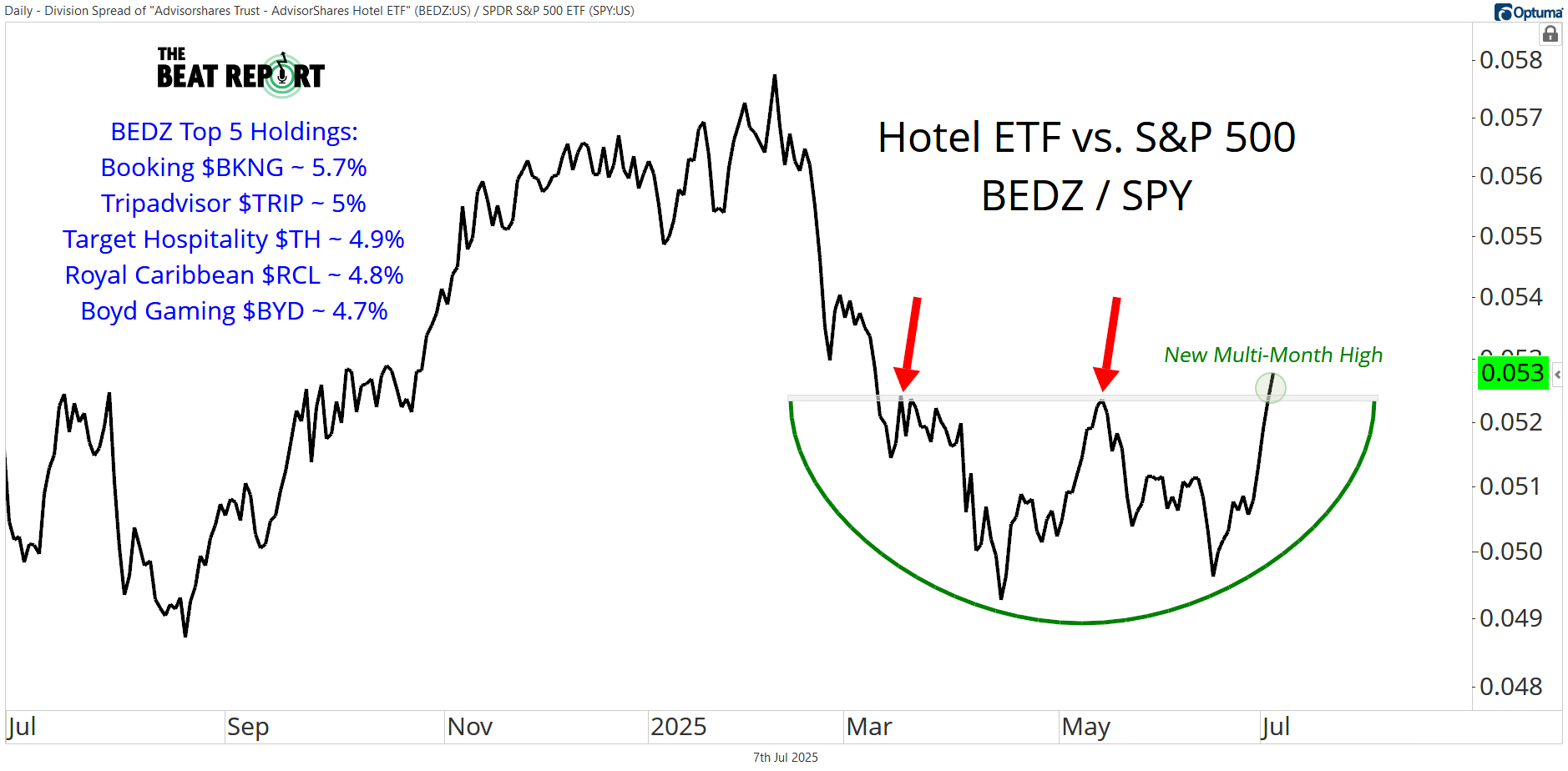

Against this constructive backdrop, hotel stocks are beginning to show signs of relative strength.

The Hotel ETF $BEDZ just broke out to fresh multi-month highs relative to the S&P 500.

We're leaning into this relative strength 📈

After a nasty drawdown earlier this year, the Hotel ETF is putting the finishing touches on a textbook bearish-to-bullish reversal pattern relative to the broader market.

This ETF provides exposure to a mix of hotel operators, travel platforms, and leisure-related companies.

Its top holdings include Booking Holdings $BKNG, TripAdvisor $TRIP, and Target Hospitality $TH.

It provides us with information on a broad range of global travel trends.

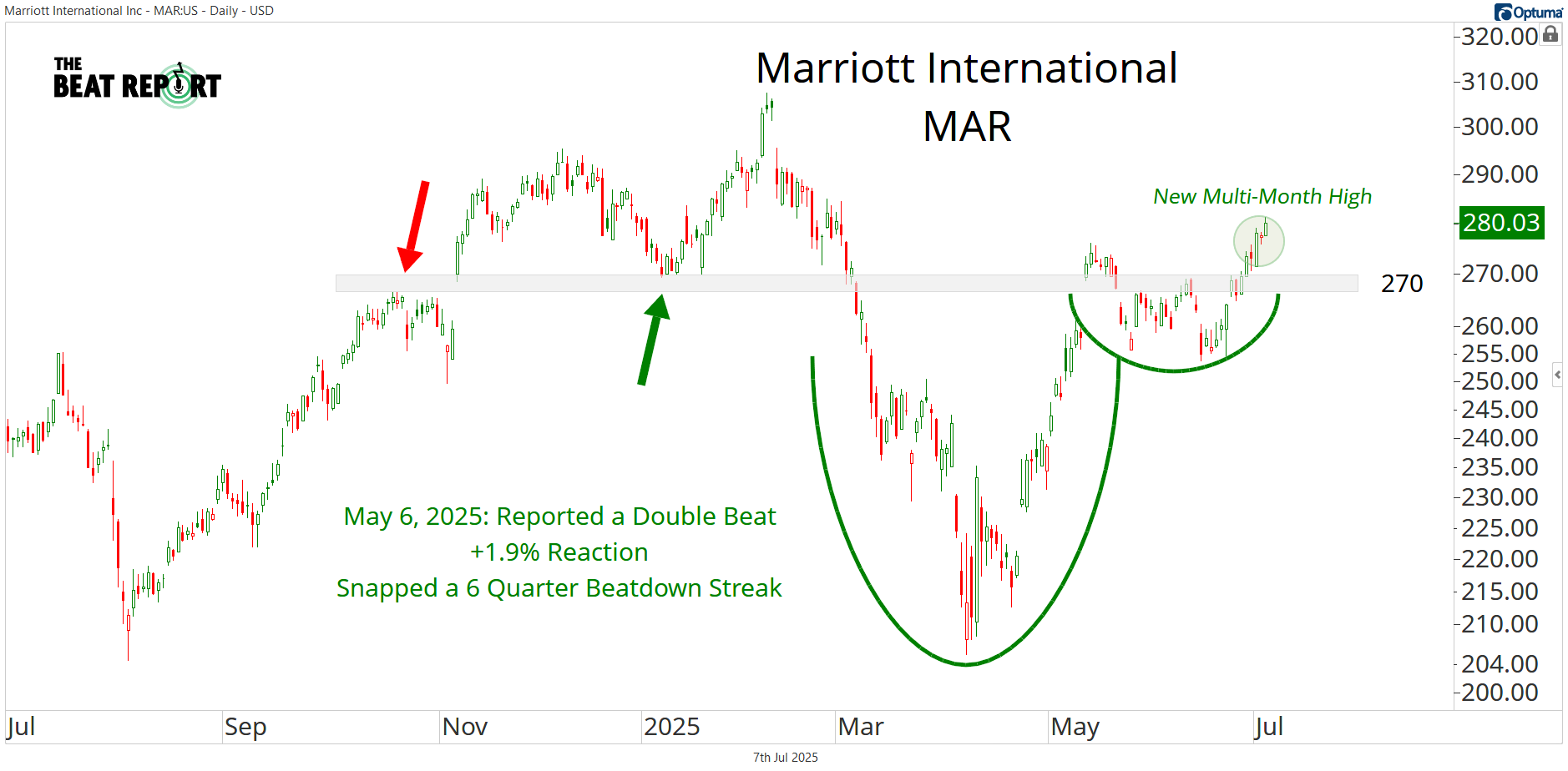

One name that stands out in this group? Marriott International $MAR.

They own and operate a large number of hotel franchises worldwide. It's the biggest and best company in the industry.

Right now, the stock is printing fresh multi-month highs.

The setup in MAR 👇

Marriott International snapped a 6-quarter earnings beatdown streak with a positive reaction on May 6.

After several weeks of consolidating recent gains, the price is making a fresh leg higher toward new all-time highs.

As long as MAR holds above 270, the path of least resistance is higher for the foreseeable future.

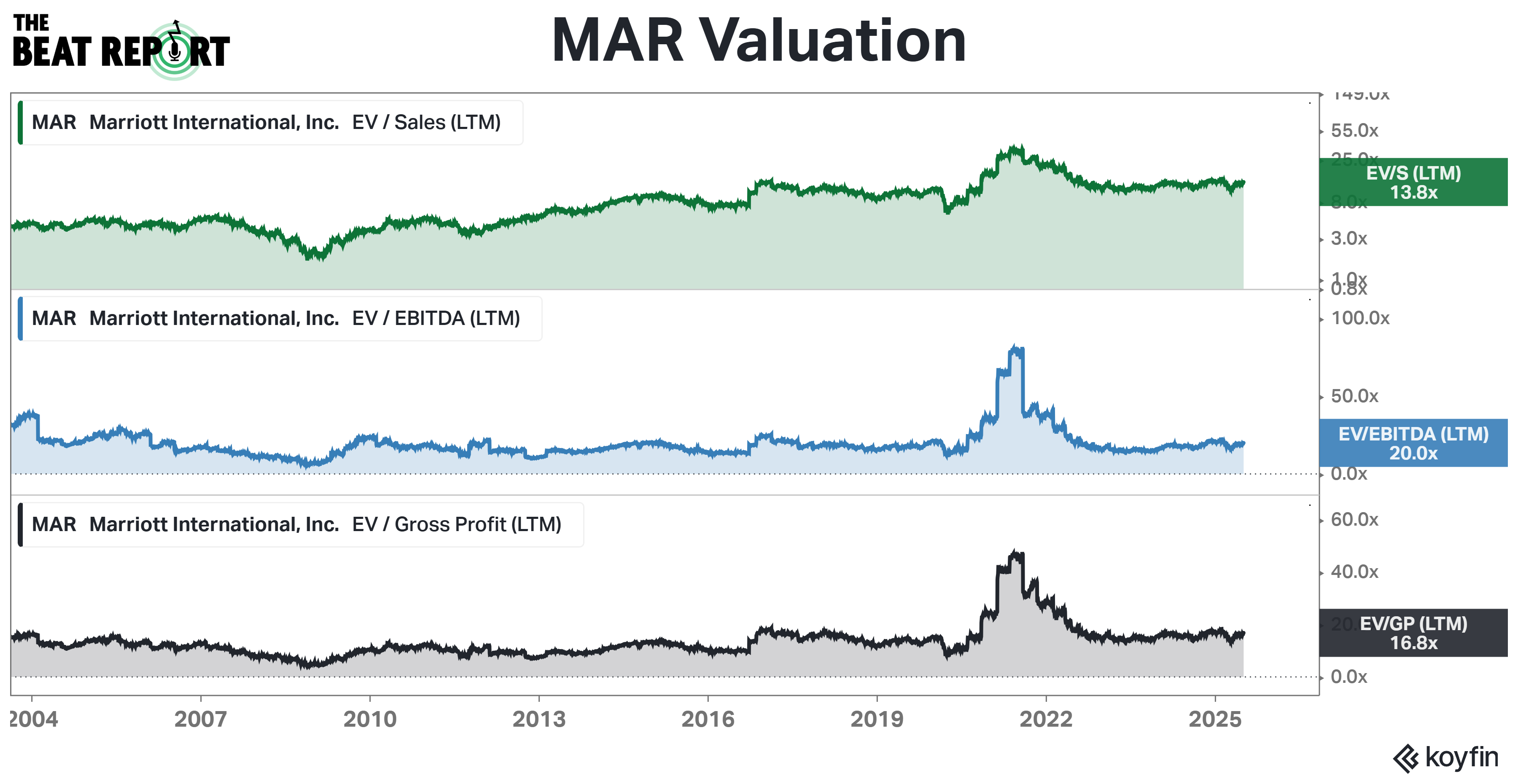

The recent breakout is occurring as valuation multiples remain reasonable.

Here's how Mr. Market is valuing MAR 👇

Marriott International achieved a record-high valuation during the post-COVID boom, but it has since returned to its long-term mean.

Its last quarterly earnings report smashed records, and we think it'll result in higher multiples for the stock.

Let's break down what happened last quarter.

Marriott reported an 18% increase in net income, alongside 5% revenue growth and 7% adjusted EBITDA growth.

What really stands out is the company’s global reach and scale:

RevPAR grew 4.1% year-over-year, with nearly 6% growth internationally and over 10% in the Asia-Pacific region.

Marriott Bonvoy, its loyalty program, has grown to 237 million members, with 68% of total room nights now tied to members (a record high).

They also added 12,200 net rooms in Q1 and announced a $355M acquisition of citizenM, a modern hotel brand targeting younger, urban travelers. This will add 36 hotels and over 8,500 rooms.

From a development standpoint, their pipeline is at an all-time high.

Margins are strong, cash flow remains solid, and capital returns are flowing, with $1B in share buybacks already completed this year and billions more to come.

We believe Marriott International is poised to become the first Lodging stock worth $100 billion.

Thank you for reading.

- The Beat Report Team

PS: Sean McLaughlin’s Options Masterclass starts Wednesday and runs for the next 8 weeks.

Learn how real options traders build smarter trades — with structure, edge, and a repeatable process.

If you find our content valuable, we would greatly appreciate it if you could shareit with your friends, family, and colleagues. Your help in spreading the word is invaluable in supporting our work. Thank you to all of you who share!